EU Foreign Subsidies Regulation increases M&A regulatory burden

Related people

Headlines in this article

Related news and insights

Publications: 26 March 2024

News: 21 March 2024

Allen & Overy advises arrangers on takeover of Encavis by KKR

News: 21 March 2024

Publications: 21 March 2024

The EU Foreign Subsidies Regulation (FSR) took effect in July 2023. It aims to regulate subsidies granted by non-EU countries to ensure that they do not distort competition in the EU internal market. For dealmakers, it is already having a major impact. The new mandatory suspensory M&A notification obligation – up and running since October – has significantly increased the regulatory burden for deals with an EU nexus.

The FSR operates alongside existing merger control and foreign investment control regimes, adding a third regulatory hurdle for merging parties to clear.

It is early days, but the regime already appears to be catching more transactions than the European Commission (EC) initially expected. The authority had estimated that around 30 deals would require notification each year. According to an EC report on the first 100 days since the start of the transaction notification obligation, the EC has engaged in pre-notification discussions in 53 cases, 14 of which have been formally notified and nine fully assessed. If notifications continue at this rate for the remainder of the year, over 50 transactions will be reviewed under the regime - 70% more than the EC predicted.

So far, the EC has not intervened in any transactions. But it has wide powers to take action against subsidies if it concludes they are distortive, including imposing remedies and even prohibiting deals.

Five key features of the Foreign Subsidies Regulation transaction review tool

- Thresholds. Companies must notify the EC if at least one of the merging parties, the target or the joint venture is established in the EU and has EU turnover of at least EUR500m, and the parties received combined “financial contributions” from non-EU countries of more than EUR50m in the three calendar years prior to notification.

- Financial contributions. These are defined very broadly and can catch transfer of funds or liabilities, the foregoing of revenue that is due (eg non‑ordinary course tax benefits), or even the purchase of goods/services by public authorities of a non-EU country or private companies whose actions can be attributed to non-EU countries. Importantly, financial contributions do not need to amount to a “subsidy” (much less one that could distort trade) to trigger notification. The EC notes that the most common types of foreign financial contribution assessed so far relate to sources of financing of the transaction.

- Timing and outcome. The review period is similar to the EU merger control process, ie 25 working days plus 90 working days (with possible extensions) for an in-depth investigation. Also like the EU merger control regime, the EC can block transactions or approve them subject to remedies.

- Fines. Failure to notify or implementing a deal during the review period can result in heavy fines – up to 10% of global group turnover.

- Below-threshold reviews. The EC can require the notification of deals falling below the notification thresholds and, separately, can investigate suspected distortive foreign subsidies on its own initiative.

Five challenges for merging parties

- Identifying which financial contributions are caught. This is not straightforward. There is uncertainty around many aspects, including tax measures and the extent to which contributions by a private entity can be attributed to a third country. The EC is providing piecemeal information on these (and other) points but has not yet issued comprehensive guidance.

- Collecting information on foreign financial contributions. This is a challenging exercise for many businesses and will be particularly formidable for those with multiple portfolio companies. Companies are grappling with how to put in place mechanisms to track foreign financial contributions on a rolling basis.

- Completing the filing form. The requirements are onerous. For example, notifying parties must submit granular data on sources of funding and a full breakdown of target valuation. While certain types of foreign financial contributions can be reported in aggregate, if disclosure exemptions do not apply then extremely detailed information must be provided. Determining whether exemptions apply can be difficult.. How far the EC is willing to grant waivers in relation to information requirements is not yet clear.

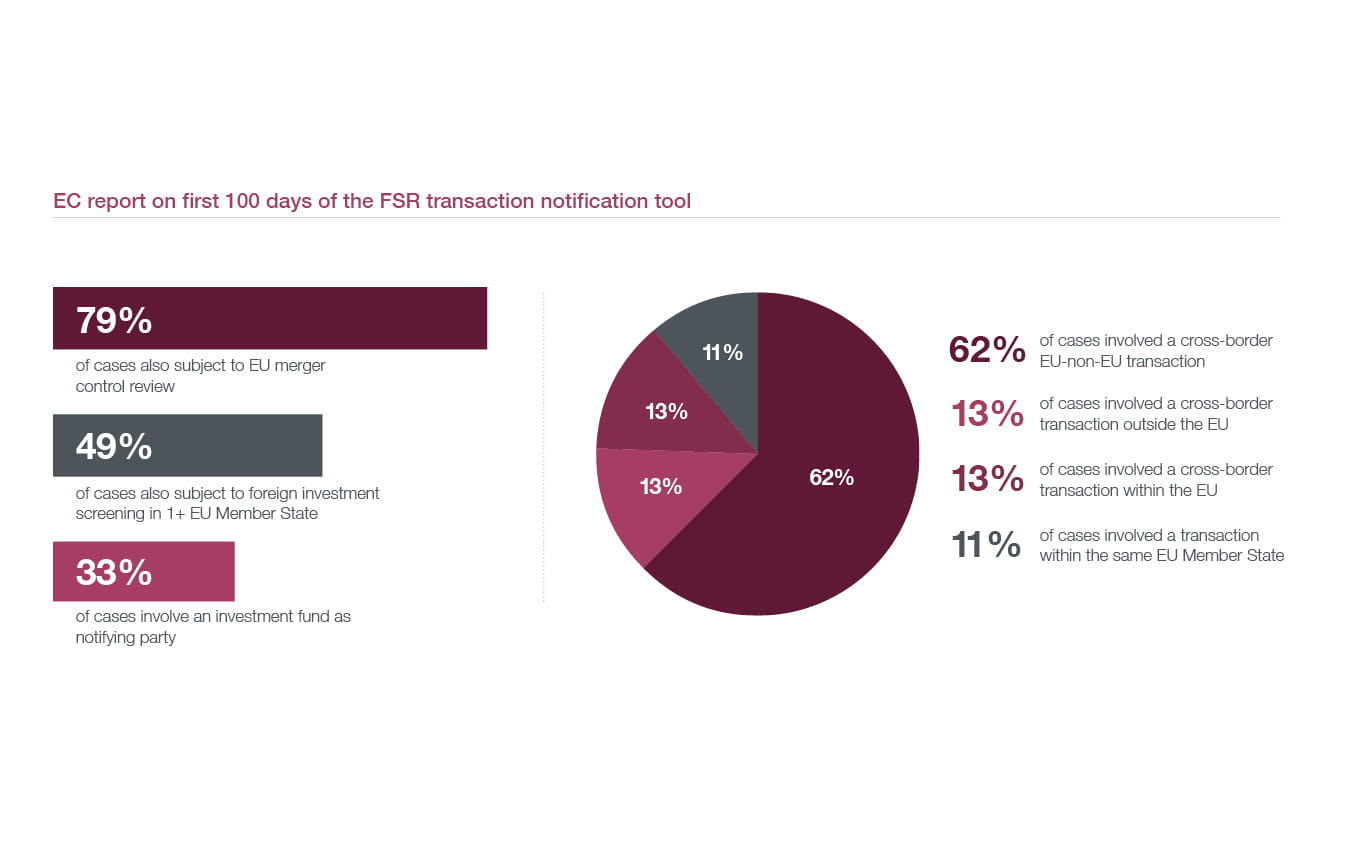

- Coordinating FSR reviews with other regulatory investigations. According to the EC, nearly 80% of FSR filings so far have been made in parallel with an EU merger control notification and around half have also been subject to foreign investment screening in one or more EU Member State. Managing and coordinating the timing of these review periods is crucial. To date we have no visibility over the extent to which EC officials working on both processes are talking to each other.

- Determining when the EC may have substantive concerns. The EC must assess whether any of the foreign financial contributions reported in the filing amount to a foreign subsidy and, if so, whether that subsidy distorts the market. The FSR sets out when a foreign subsidy is most likely to be distortive (eg when it directly facilitates a transaction) and enables the EC to balance positive and negative effects. However, the EC has not published guidelines on how it will carry out this assessment in practice.

The upshot

For all transactions with an EU nexus, the applicability of the FSR must be considered at the outset. A transaction risk analysis should be carried out alongside merger control and foreign investment assessments. If a filing is required, appropriate conditions should be included in transaction documents and the deal timeline should account for the EC’s review period.

Foreign subsidies are also on the radar of the U.S. antitrust authorities.

Reforms to the HSR filing form will require parties to submit information on subsidies received from certain governments or related foreign entities. The scope of the data required appears to be narrower than under the FSR. But parties should consider ensuring that any system set up to identify FSR disclosure requirements is also designed to collect information for U.S. merger filings.