Latest attestations numbers: Has the novelty worn off for the FCA?

Browse this blog post

If the FCA’s supervisory tools were toys, attestations would be near the top of the ‘most wanted’ list. Indeed, the FCA has made no secret of the fact that it considers attestations to be a particularly effective supervisory tool and that it has been requesting attestations from senior individuals within firms with increasing frequency.

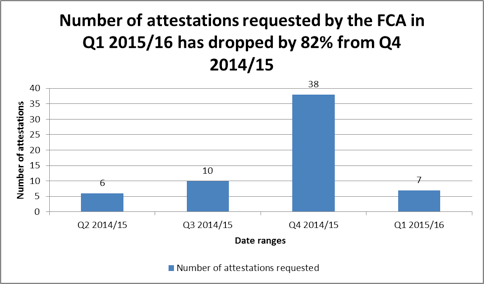

However, this makes the latest figures published by the FCA yesterday regarding attestations all the more curious. During Q1 of 2015/16, the FCA only requested seven attestations, a decrease of 82% from the previous quarter.

Of the seven attestations requested by the FCA in Q1 2015/16, three related to retail issues, a further three to wholesale and investment management issues and one related to general insurance and protection issues. This ‘spread’ of attestations is consistent with historic patterns. According to data published by the FCA, since 2013/14 by far the most attestations (71 in total) have been requested by the FCA in relation to retail, wholesale and investment management issues.

So why the drop in the number of attestations?

The FCA has provided no commentary to explain the drop in the number of attestations it requested during Q1 2015/16, nor did it for the apparent spike in the number of attestations it requested during Q4 2014/15. It is possible that during Q4 2014/15 the FCA went out to a number of firms to request attestations from senior individuals in relation to one or more particular subjects, thereby resulting in an unusually larger number of attestations being requested.

Whatever the reason for the fluctuation in the number of attestations requested, the low number of attestations requested by the FCA in Q1 2015/16 is unlikely to be a sign that the FCA’s appetite for using attestations is waning. This is especially so given that the FCA sees attestations as an effective way of focusing senior management’s attention on key issues and requiring them to personally confirm that a particular action has been taken, or that an issue has been resolved.

An enforcement perspective

When attestations were first introduced, it was anticipated that the FCA may use attestations as a basis for taking enforcement action against senior individuals within financial institutions. For example, if a senior individual gave an attestation which later turned out to be inaccurate, the FCA may consider taking enforcement action personally against the senior individual concerned for breaching one or more provisions of the Statements of Principle and Code of Practice for Approved Persons (APER).

Several years after the FCA started to formally use attestations, we are yet to see enforcement action taken against an individual that is based on an attestation they provided to the FCA. However, this is not to say that the FCA has not got its sights set on taking up such a case in the future. In addition, the FCA’s ability and confidence to bring such enforcement action may increase once the new Senior Managers Regime comes into force from March 2016 as the Presumption of Responsibility will make it easier for the FCA to take enforcement action against Senior Managers.

Source of data: FCA website.