SPACs listings in Hong Kong – a comparison among different jurisdictions

Related people

Headlines in this article

Related news and insights

News: 25 September 2023

Allen & Overy advises on LC Logistics’ listing on the Hong Kong Stock Exchange

Publications: 02 March 2023

China refreshes the regulation on archives administration in relation to overseas listings

Publications: 17 October 2022

Private placements and other exempt offerings in Hong Kong: Overview

On 17 December 2021, the Hong Kong Stock Exchange (HKEX) published consultation conclusions allowing the listing of Special Purpose Acquisition Companies (SPACs) in Hong Kong. This follows the publications of new rules on SPACs listings in other jurisdictions, including Singapore and the UK.

In 2021, the total number of initial public offerings (IPOs) of SPACs in the U.S. was more than ten times the total number of such IPOs two years ago in 2019. In the European SPAC market, a number of SPACs have recently been listed, in particular in the Netherlands. With the SPACs boom in the last three years, different jurisdictions, including Hong Kong, have started to establish a listing regime of SPACs in order to maintain their competitiveness as fundraising hubs in the global market.

A SPAC is a shell company without prior operating history and revenue-generating business. It raises funds through an IPO process which will be used to combine with a target operating company, typically referred to as a ‘de-SPAC’ transaction. If a de-SPAC is successful, the target company will then achieve public listing. If a de-SPAC is not successful prior to the prescribed deadline, the SPAC has to be liquidated and funds raised have to be returned to investors.

SPACs in different jurisdictions

SPACs were conceived in 1993 and have seen a spike in popularity in recent years. According to the statistics published by SPACInsider, in 2020, SPACs have raised USD83.4bn from 248 IPOs in the U.S. market. There has been a substantial growth in the popularity of SPACs in 2021, and by mid-December there were already 603 SPAC IPOs raising USD160.9bn.

In view of this SPACs boom, different jurisdictions have amended their regulations in order to keep up with the market trend for fundraising. In the U.S., the Securities and Exchange Commission has issued various new forms of guidance concerning disclosure and accounting treatment and continues to scrutinise SPACs. Regulators and stock exchanges in other countries across Europe and Asia — including Euronext (notably Euronext Amsterdam) and the exchanges in the UK, Singapore, and Indonesia — are also jumping on the bandwagon to review their current listing rules and allow SPACs listings, proposing rules similar to those in the U.S.

The Singapore Exchange Regulation has issued its finalised rules for SPAC listings on the Mainboard of the Singapore Exchange following a public consultation. The new rules took effect on 3 September 2021.

The European SPAC market, in particular in the Netherlands, has developed because it may be challenging to merge an EU target with a U.S. SPAC, owing to the effect of cross-border tax rules, specifically the U.S. anti-inversion regime. In addition, U.S. SPACs will typically be U.S. listed and the enlarged group may prefer to avoid perceived litigation risk and the enhanced regulatory burden associated with a U.S. listing. The European SPAC marries U.S. SPAC features with the EU regulatory environment, except that the IPO proceeds are put into an escrow rather than a trust fund.

For the UK, previously there was a presumption in the UK Listing Rules that the listing of a shell company will be suspended at the time when the target company is identified. On 30 April 2021, the Financial Conduct Authority published a consultation paper on SPACs listings, and on 27 July 2021, it published the final changes to the UK Listing Rules applicable to SPACs which took effect on 10 August 2021.

SPACs in Hong Kong

In March 2021, the HKEX and the Securities and Futures Commission (SFC) were invited to explore the introduction of a SPACs listing regime to enhance the competitiveness of Hong Kong as an international financial centre.

The HKEX published a consultation paper in September 2021 seeking feedback on proposals to create a listing regime for SPACs in Hong Kong. The consultation period ended on 31 October 2021.

On 17 December 2021, the HKEX published consultation conclusions and decided to implement the proposals outlined in the consultation paper broadly as proposed, with minor modifications to reflect comments received. The new rules will come into effect on 1 January 2022.

Under the Hong Kong SPACs listing regime, the key criteria are:

Pre de-SPAC

- Subscription for and trading of SPAC’s securities will be restricted to professional investors only. However, this restriction will not apply to trading of the successor company shares (post de-SPAC).

- SPAC shares and SPAC warrants must be distributed to a minimum of 75 professional investors, of which 20 must be institutional professional investors.

- Promoter shares should be capped at a maximum of 30% of the total number of all shares in issue as at the initial offering date.

- SPAC promoters must meet suitability and eligibility requirements, including each SPAC must have at least one SPAC promoter which is an SFC-licenced firm holding at least 10% of the promoter shares. The HKEX will consider granting waiver on a case-by-case basis (for example, to accept a SPAC promoter if they have overseas accreditation that is equivalent to an SFC licence).

- Any material change in SPAC promoters would require approval by special resolution of shareholders (excluding the SPAC promoter and close associates).

- The funds expected to be raised by a SPAC from its initial offering must be at least HKD1bn (USD128m).

De-SPAC

- A successor company must meet all new listing requirements (including IPO sponsor engagement to conduct due diligence, minimum market capitalisation requirements and financial eligibility tests).

- A de-SPAC transaction must be made conditional on approval by SPAC shareholders at a general meeting, which would exclude the SPAC promoter and other shareholders with a material interest.

- SPAC shareholders must be given the option to redeem their shares prior to a de-SPAC transaction.

De-listing

- If a SPAC is unable to announce a de-SPAC transaction within 24 months, or complete one within 36 months, the HKEX may suspend the trading of the SPAC. The SPAC must, within one month of the suspension, return 100% of the funds that it raised (plus accrued interest) to its shareholders. The SPAC will then be de-listed.

The Hong Kong regulators try to strike the balance between investor protection and market attractiveness.

Those supporting SPACs listings hold the view that allowing SPACs is a necessary move to boost Hong Kong’s competitive edge to attract investors, as Hong Kong has already fallen behind Singapore and other jurisdictions.

However, introducing SPACs may give rise to the concern that this mechanism may be used to achieve backdoor listing and circumvent the asset quality and suitability requirements applicable for normal listing applicants. The HKEX has been reluctant to allow backdoor listings and has recently tightened the listing rules to prevent the listing of low-quality assets. Apart from SPACs listings, the listing of certain investment companies without actual business is permitted under Chapter 21 of the listing rules. The key difference is that a Chapter 21 company is not allowed to own more than 30% of another company, whereas a SPAC can have full control of the investee. Also, a single investment must not exceed 20% of the Chapter 21 company’s net asset value.

The HKEX intends to ensure that the SPAC listings have experienced and reputable SPAC promoters that seek good quality de-SPAC targets. The HKEX’s SPACs listing regime is more stringent than that of the U.S., owing to the fact that there is a proportionately higher retail market participation in Hong Kong than in the U.S. The U.S., UK and Singapore all have regimes that do not limit investment in SPACs (prior to the completion of a de-SPAC transaction) to professional investors, while Hong Kong has such requirement. Under the HKEX listing regime, SPAC promotors must meet suitability and eligibility requirements, and each SPAC must have at least one SPAC promoter to be a firm that holds a Type 6 (advising on corporate finance) and/or a Type 9 (asset management) licence issued by the SFC (unless the HKEX waives such requirement based on the merits of the case).

The successor company will need to fulfil new listing qualification requirements as for a traditional IPO, including the requirement to appoint an SFC-licenced IPO sponsor to conduct comprehensive due diligence, similar to the UK SPAC regime which requires a successor company to fulfil full eligibility and listing requirements on a de-SPAC. Further, a de-SPAC transaction must be made conditional on having obtained the HKEX’s listing approval. The de-SPAC rules are not dissimilar to those which govern reverse takeovers under the HKEX listing rules.

The de-SPAC transaction must be made conditional on approval by SPAC shareholders, and the SPAC promoters and their close associates must abstain from voting at the relevant general meeting. This is similar to the UK where shareholders’ approval is required and founding shareholders are prevented from voting.

This has been a difficult balancing act for Hong Kong’s regulators. On the one hand, sufficient safeguards (such as minimum market capitalisation requirements and mandatory redemption rights) should be imposed to give protections to investors; on the other hand, over-regulation will restrict flexibility, the core feature of the SPACs listing regime.

The HKEX believes the introduction of the SPAC listing regime is in line with the HKEX’s strategy to remain a competitive international financial centre that can continue to attract Greater China and South East Asia companies to list in Hong Kong.

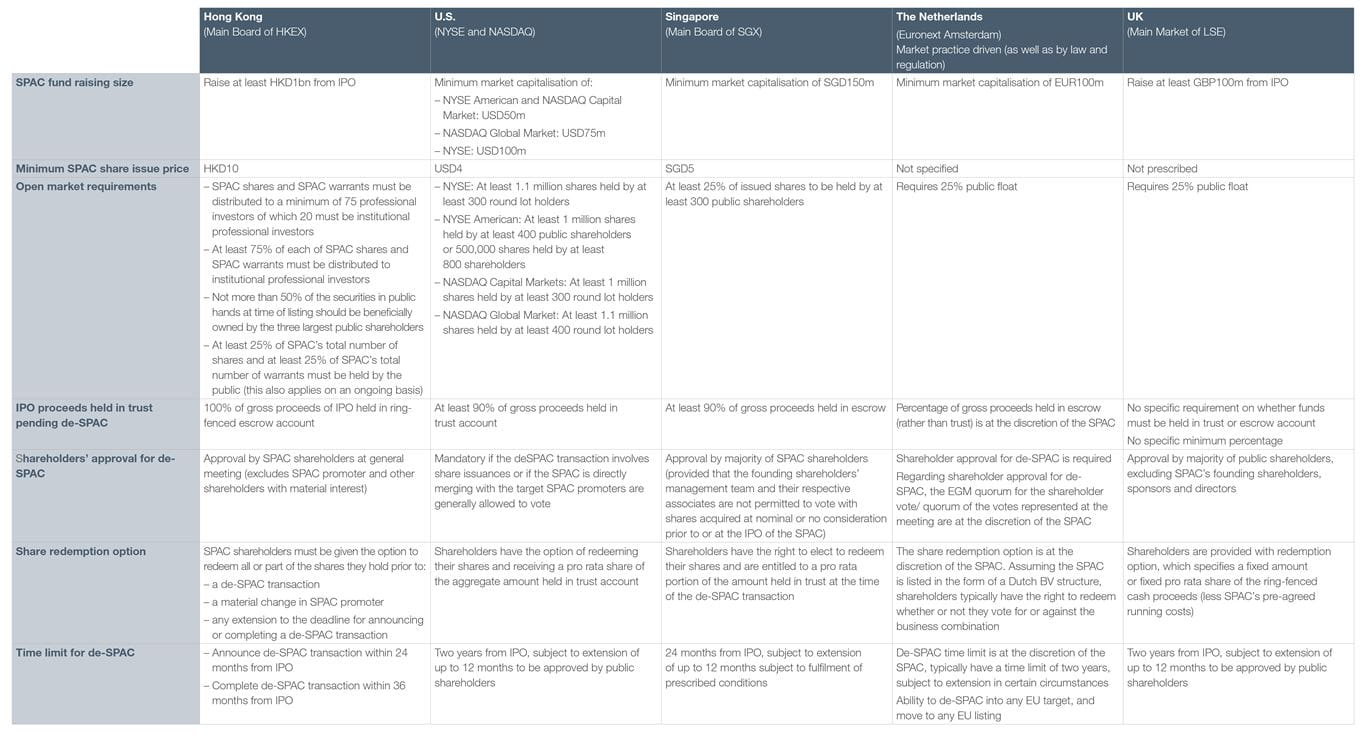

Comparison of SPACs listing framework among different jurisdictions

The table below sets out a comparison of Hong Kong’s SPACs listing regime against the current regimes of the U.S., Singapore, the Netherlands and the UK: